Third Quarter 2025: Geopolitical Drama Stresses Metals Markets

Our Markets & Metals feature of Wreckonomics™ series reports on the market performance and the underlying opportunities and stressors for the commodities & supplies derived from Recycled Vehicles. Market performance in the second quarter of 2025 saw influences of global trade disagreements and shifting supply dynamics impact our partner landscape in several ways. We’ll be watching these forces closely but we further expect the continued increase in new vehicle prices, and potentially longer retention of older vehicles due to these prices, could also influence the flow and value of end-of-life vehicles and effect pricing

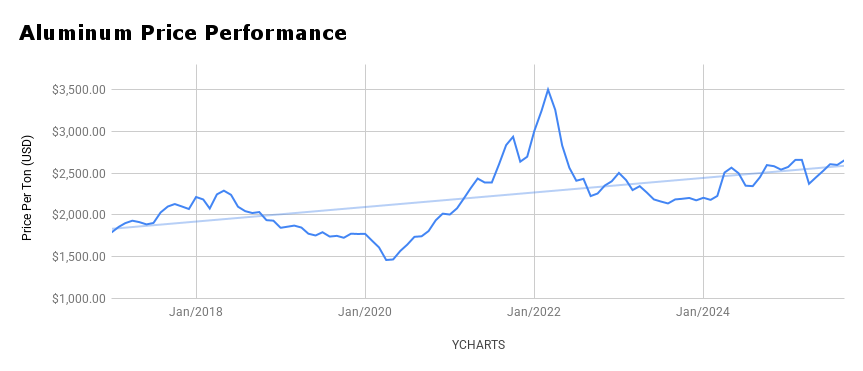

Aluminum

Aluminum performance in Q3 2025 was marked by global price stability on the futures market, offset by historic premiums in the U.S. Throughout the quarter, The London Metal Exchange (LME) aluminum spot price fluctuated around the $2,580 to $2,660 per metric ton range, suggesting the market found a temporary equilibrium. This stability was supported by solid cost factors, such as high aluminum prices, and long-term bullish expectations of a supply deficit heading into 2026.

Domestic demand and U.S. Market: The U.S. Midwest Premium reached a historic high, a massive increase since late 2024, reflecting tightening domestic supply due to tariffs and restricted import flows. This domestic price surge creates a significant cost headwind for U.S. manufacturers using recycled aluminum.

Outlook: While the global outlook points to a supply shortfall, the high U.S. premium remains a key stressor. These tensions could create a risk of demand destruction in the domestic market.

Rare Metals Market

In automotive recycling the most valuable minerals retrieved are mainly derived from recycling of Catalytic Converters. These environmental warriors often contain Platinum, Palladium and Rhodium specifically. The presence of these rare metal nanoparticles act as a ‘catalyst’ and help to convert hydrocarbons, carbon monoxide and oxides of nitrogen into less harmful carbon dioxide, nitrogen and water vapor. For over 40 years Catalytic Converters have been the ‘big gun’ and most impactful contributor to the efforts to reduce carbon emissions from internal combustion vehicles. Unfortunately their small but important contributions have never been able to fully offset or arrest carbon emissions entirely but the continued use and regulatory requirements make the markets for these rare metals remarkably important benchmarks.

Palladium

This metal should continue to face long-term downward pressure from the rising market share of Battery Electric Vehicles (BEVs), which displace internal combustion engine (ICE) and hybrid production, and the substitution of palladium with cheaper platinum in some applications.

In Q3 Palladium had a modest rebound & some volatility, starting very strong and then losing momentum. Prices found support from short-covering and renewed supply concerns, particularly due to ongoing Russian and South African supply risks.

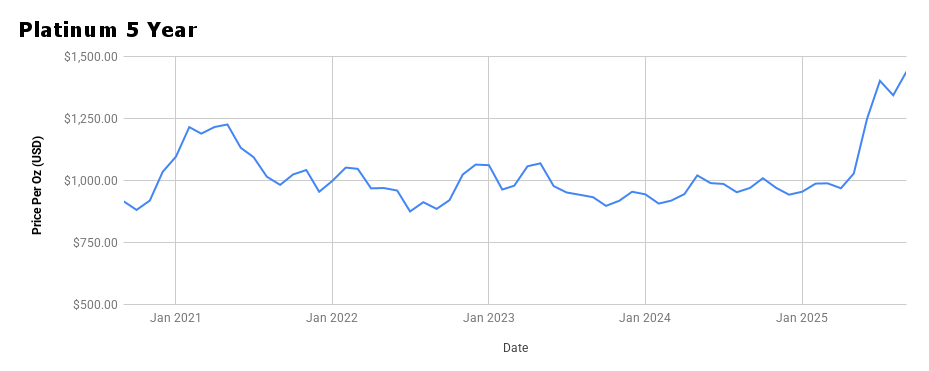

Platinum

As the outstanding performer in Q3, Platinum showed continued strength. Following its Q2 surge of almost 25%, Platinum prices remained exceptionally strong, up by almost 48% YOY by the quarter’s close.

The primary driver remains the ongoing production deficits in South Africa (the world’s largest producer), due to heavy rainfall and ongoing infrastructure challenges, and reduced output from Russia due to sanctions. Demand from the jewelry sector also saw an increase, as manufacturers began using platinum more due to high gold prices related to consumer behaviors.

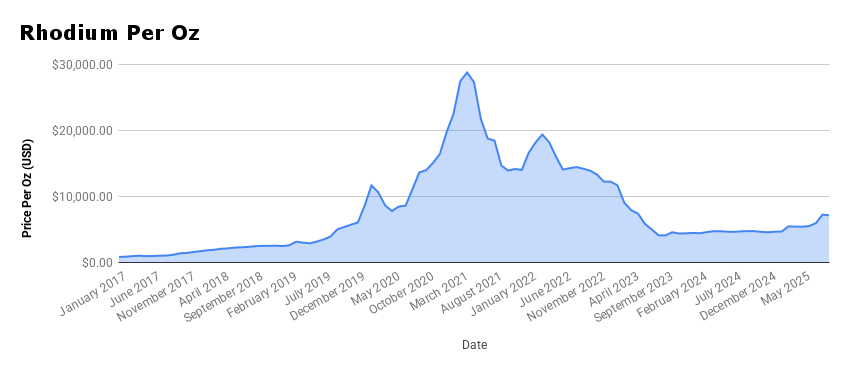

Rhodium

Once again, let’s check in on the star of the pandemic circus: RHODIUM. Every year approximately 30 tons of Rhodium is used in Catalytic Converters. Approximately 30 – 50% of this comes from recycling. During the pandemic rhodium scarcity caused a giant spike in prices, and led to huge increases in Catalytic Converter costs and also surely inspired a uptick in converter theft. In Q3 Rhodium remained strong. Price strength is continues to be supported by a severe supply deficit. Forecasts suggest the deficit for 2025 will reduce above-ground stocks to their lowest level in over 40 years, leaving the market acutely susceptible to physical market squeezes and large price swings.

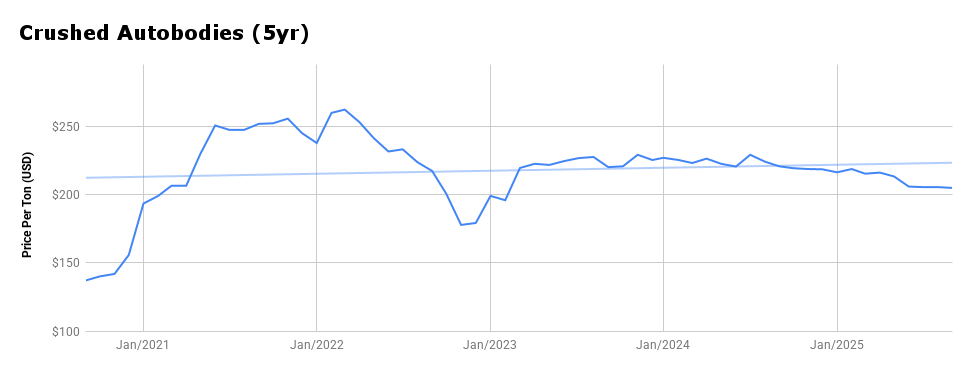

Crushed Auto Bodies

The most significant indicator of end of life vehicle demand is the sale of whole ‘auto hulks’ processed (environmental handling, parts, cores and rare metals retrieved) by auto recyclers to shedding operations for production into recycled content. The primary raw material is the ferrous metals found in these crushed autos. For Q3 there was very little price movement, however, year over year the values are down approximately 10%.

The expected trickle of domestic tariff protection and increased infrastructure/manufacturing demand may be beginning to impact prices. However, volatility remains high, and the overall performance for auto scrap segments has not returned to the multi-year highs seen in early 2024.

.

Source: Advanced Remarketing Services

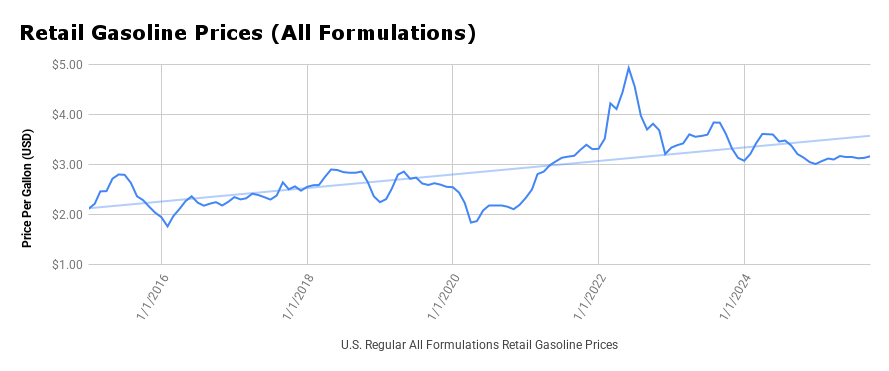

Fuel Prices

The favorable trend in fuel costs, a critical factor for transportation and logistics, held steady through the third quarter. The national average price for regular motor gasoline remained relatively stable and generally low for a summer period. This stability provides a continued welcome relief for transportation-reliant industries, including vehicle remarketing and scrap hauling, mitigating some of the logistics cost pressures that plague other parts of the supply chain.

Overall, Q3 2025 presented a complex picture defined by diverging paths: precious metals were driven by tightening supply and geopolitical risk, while bulk metals (steel, aluminum) faced a tug-of-war between high domestic premiums (aluminum) and very modest growth in scrap demand (steel). The overarching influence of high vehicle prices continues to shape the availability of ELVs, forcing recyclers to maximize value from a supply stream under constraint.

If your organization has a consistent volume of low value, high mileage and older vehicles, we should talk. Reach out to any of our team directly or email us at arsinfo@arscars.com